Equity Capsule: Curated weekly: #E2

Equity Capsule: Curated weekly: #E2

What makes stocks go up (and down), some takeaways from RIL Annual Report searching for growth, India-China trade face-off, Li Lu, market predictions and more..

Welcome back - hope you enjoyed the first edition of Equity Capsule. In case you missed, you can check here

As you see, the newsletter is now “weekly”, given time limitation during the week to write a decent note. With that little bickering and an apology, let’s get on with it!

#1 The Anatomy of Stocks That Go Up (and Down)

Came across the promising Dubra's substack- (focused on US markets, but written with universal investing principles) and this one particular post caught my fancy. While there is a tomb written what leads to outsized returns over time and what forms investment traps, Dubra does a good job at bringing it down to one post. I’ve made this handy visual summary :

As with anything in investing, there is a no one-size fits all approach. A good way to look at stocks that ‘may’ go down is to look for combined cues (for example -High debt + high Operating leverage). Of late, TVS Motors moved out of my watchlist due to this combination.

Management quality is a layer that needs to be super-imposed at all stages of evaluation. Would recommend one to spend more time on other posts on the blog to understand better. Good reads.

#2 Some takeaways from Reliance Ind. Annual Report

To put it mildly, RIL owned this lockdown like a boss. With 12 funding deals across 11 weeks amounting to ~1.2 lakh crores, it has moved in it’s own stratosphere. Not surprisingly, some call it India’s answer to US FAANG big tech stack.

At 43.2 MB and 460 pages, it is by far the heaviest AR (second is Polycab at 26 MB). Clearly, reading between the lines will take more time and effort, so let’s look only at key highlights:

RIL FY20 AR provides good insights into transition of a traditional company (O2C) to a digital company

All the building blocks in place to build a behemoth – R&D, Capex, brands, offline and digital strategy, supplier and customer networks, and human capital.

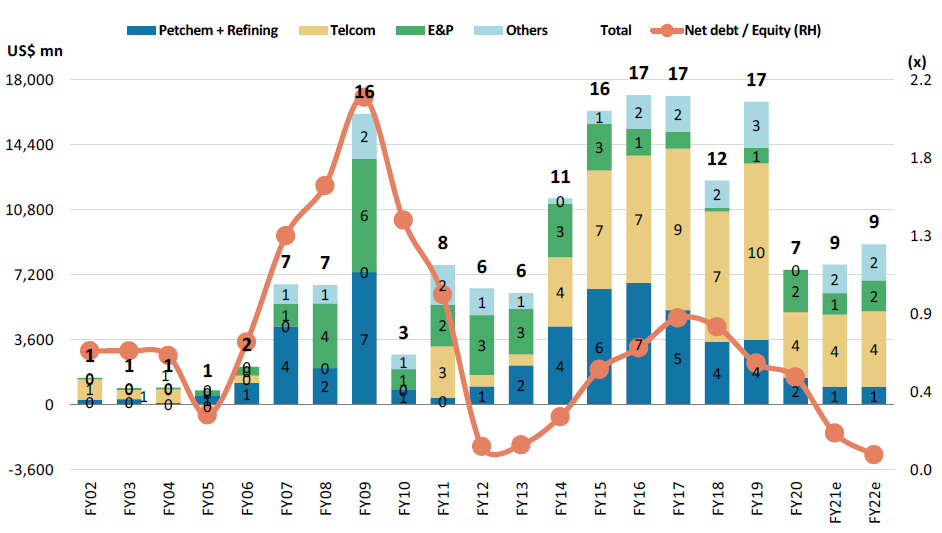

Capex Cycle and Deleveraging:

RIL has been in an aggressive capex cycle in the last 5 years, leading to a subdued ROCE and ROIC. Sometime back, there was an interesting analysis by Zaid Munshi on Twitter that RIL has been unable to beat it’s Cost of Capital. Had tried pointing out on the CWIP (unsubstantiated capex) might be a reason, but the picture was still a little fuzzy in my mind:

As per management, Capex is largely completed for Jio with formation of Jio Platforms; and the focus has shifted to Jio Fiber (the AGM on July 15 might focus on this) and creating solutions ecosystem for digital services.

Let’s see how RIL funded it’s huge capex of ~5 lakh crores between FY16 and FY20 (chart via Morgan Stanley):

Interesting to see, almost 60% was funded via internal cash generation (thanks to Petrochem) and only 15% (~INR 77,000 Cr) via borrowings. Thus, achieving net Debt free status before committed timelines in last last AGM adds up. Deleveraging process in chart via Axis Capital:

Bonus: RIL investment cycle chart over the years via MS. Note, they do not estimate large capex going forward.

And thus an uptick in the subdued return profile in the future:

Note: Not to be construed as an investment advice at current levels.

Petrochem:

Working to complete the contours of a defining strategic partnership with Saudi Aramco (Aramco), and both companies have the goal of increasing Oil to chemicals integration. Refinery complexity was 21.1 in FY20 for Jamnagar, up from 12.7 in F19, with the start of integration projects in chemicals. The company highlighted its vision of becoming one of the top five petrochemical companies in the world.

Retail - ‘Fiber to Wardrobe':

RIL had 64 cr footfalls at 11,784 stores across 1,800+ cities and towns in F20.

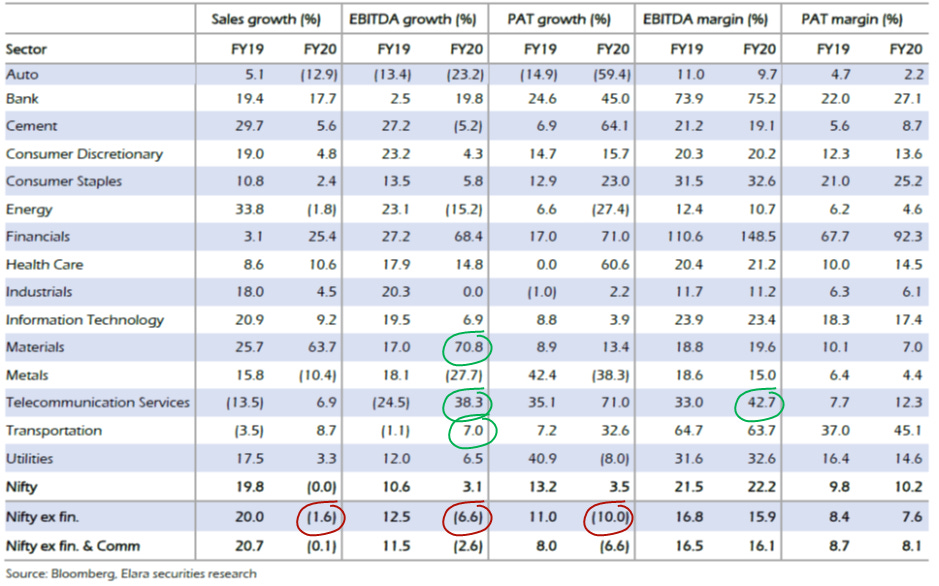

#3 Where was the growth anyway?

An Elara report shows ex-financials growth and profitability had already been in negative territory before the COVID wave..

Industry wise performance of Nifty stocks in FY20 versus FY19:

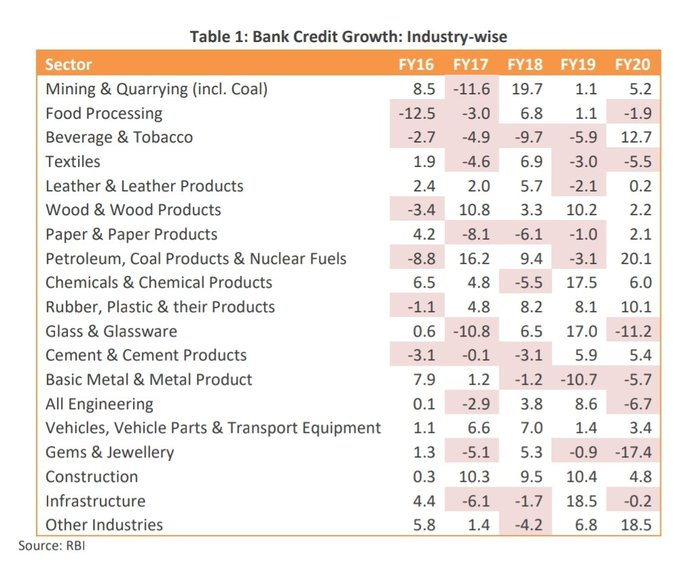

And where have the Banks been lending? I see some sectors now out of favor, but still hot in investment community. May be I am looking with a tinted “glass”..

(Source: CARE Ratings report)

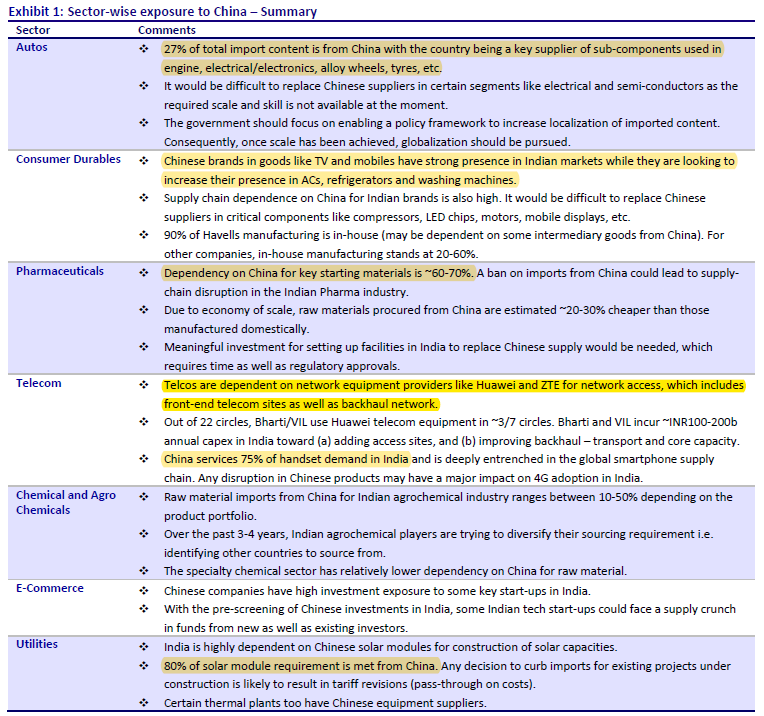

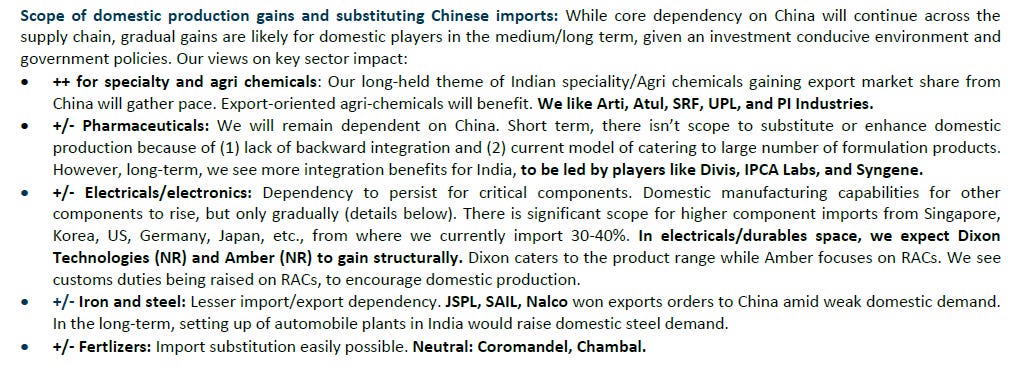

#4 India-China: The myth of import dependence (click)

The mastery of Rathin Roy on economy is well known. Dr. Roy argues that contrary to popular opinion, China dependency is very much replaceable (maybe slightly more expensive), except for few critical areas in electronics and pharma.

A Motilal Oswal report provides summary of key imports from China and sector wise exposure and impact:

Here is what a Philip Capital report suggests on the same:

Atmanribhar Bharat is likely to receive an early push from India’s ongoing geo-political tensions with China. As per channel checks with policymakers, excessive trade dependency on China will certainly REDUCE in coming months/ years through incentivizing domestic production and import substitution. While this would create near to medium-term production/cost challenges in the supply chain, some domestic companies should benefit. For critical components, China will remain the key supplier, due to lack of technical competence/ investments by the Indian manufacturers and government support.

Amongst the large import sectors, core dependency is expected to persist for pharmaceuticals and critical electricals/ electronics/ machinery (EEM). Indian companies can develop capabilities for speciality/ agri chemicals, EEM, and fertilizers. Import substitution is likely for iron & steel, fertilisers, EEM.

Areas where Philips expects India to gain over medium and long term:

#5 Notes from Li Lu’s Columbia address , 2006

If you are like me, your bookmarks tab keeps piling up - there is always so much happening. I am glad to have visited this bookmarked talk from couple of weeks back (H/T: Gautam Baid and Jitendra Chawla for the heads-up). An absolute value investors’ delight (Note: Video starts around the 6 minute mark)

For the uninitiated, Li Lu is a Chinese immigrant in US who manages a large fund called Himalaya Capital. Video profile: Li Lu

In the words of Charlie Munger:

“I’m 95 years old. I’ve given personal (Munger) money to some outsider (anyone beside Warren Buffet) to manage once in 95 years. That’s Li Lu.“

With that good enough reason for picking up this talk, let’s straight jump into key takeaways:

Value investing thought process comprises only 5% of the market. It is tempting to do what the other 95% of people do. Biggest challenge is to understand whether you are the 5% or the 95%.

Does not care where something traded before. First looks at valuation - if the valuation doesn’t fit, doesn’t go beyond it. If you see a low P/B ratio, ask – What is in the book? How much is the book?

Look at pre-tax and pre-interest earnings. Look from an un-leveraged basis. Figure out how much capital is deployed in the business. Look at ROIC.

Management due diligence: Li Lu describes his diligence process before taking a (big) position in Timberland (the company that makes these rugged shoes in image).

Low key, closely held business. While there were temporary growth outlook challenges related to the Asian Financial crisis, traded cheap at around book value (5x P/E), despite having grown well and decent profitability. But zero analyst coverage - clearly not liked by Wall Street. A good case of Balance Sheet to Income statement investing:

Gains can be even greater if the company’s current investors are paying a multiple of book value, but future investors are willing to pay a multiple of earnings, or cash flow, or EBITDA.

Li Lu flew out to the neighbourhood of the owners, joined overlapping boards to meet the son (COO of company), and became intimate friends with the owners family. All this to see how the management conducts their daily lives and business philosophy. Got comfort, allocated big and made a cool 50x+.

The point here is that it takes a certain amount of hard work and obsession to “really succeed big" in investing. Taking shortcuts is tempting, but nowhere as rewarding.

Some other takeaways:

Have a high bar for the margin of safety. You don't have to buy a "maybe". Your productivity in a year is not determined by how many stocks you bought, but what you learned.

Let curiosity and passion drive your work, get boots on the ground and do the kind of research others don't think to do.

Have confidence in the niche you've carved out. Even the best investors can't compete with you if you look where they don't and think the way they don't.

Bonus: Here is Li Lu on importance of culture in business:

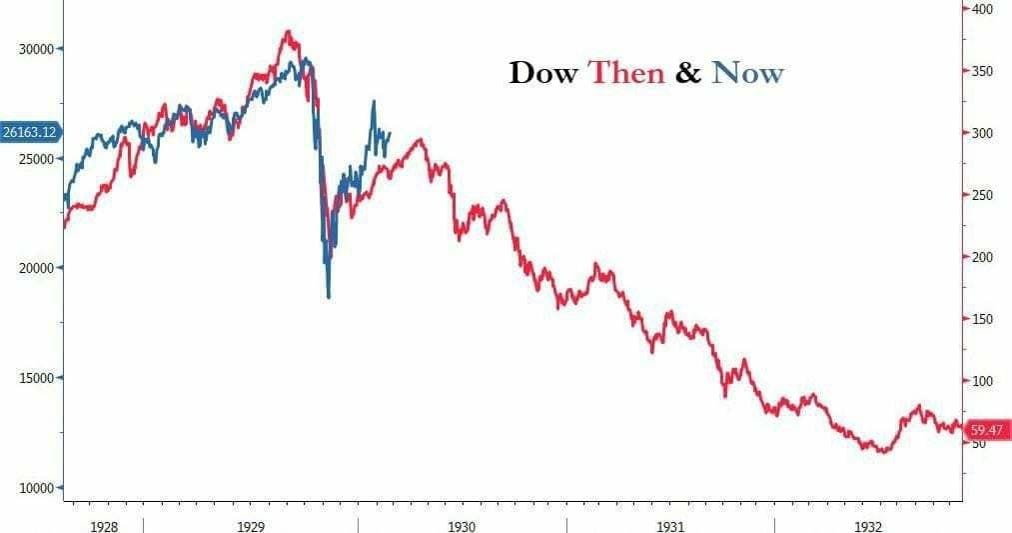

#6 Market predictions - The Up , down and the sideways

“History Doesn't Repeat Itself, but It Often Rhymes” – Mark Twain.

The speculation market is hotter than before. Came across few extreme opposite charts on possible market directions, which I found amusing :)

The 1929 crash scenario..

The 2009 fierce recovery scenario

And the sideways theory as FED takes a breather..sigh!

I don’t know which way we are heading, so might as well..

If I may suggest a good read: Expectation and Reality: The Stock Analyst of 2050

Suggested readings:

Some of the most influential essays of our times via Patrick OShaughnessy

On APIs and Deepak Nitrite:

Quick FY20 vs FY19 Balance sheet review (brilliant compilation):

A handy list of companies in capex phase:

That’s all for now folks..CIAO!

I like it!

Thoroughly enjoyed it! Very insightful. Waiting for more.